Investment Insights: Embracing Asset Class Strategies with Apollo Lupescu (Ep. 140)

Larry Heller, CFP®, CDFA ® welcomes Apollo Lupescu, Vice President of Dimensional Fund Advisors, a prominent global investment management firm to discuss the emotional and logical thought process associated with investing. Listen as Apollo delves into the distinctive investment approaches employed by Dimensional Fund Advisors, placing significant emphasis on their meticulous data analysis and their commitment to asset-class investing. The conversation also touches on the significance of effectively managing your investment expectations, the merits of diversification, and gaining a deep understanding of market probabilities.

Watch the Video Version

Listen to the Audio Version

“Swimming with a school of fish”, that’s how Apollo from Dimensional Fund Advisors describes asset class investing in this episode of Life Unlimited.

Larry Heller, CFP®, CDFA ® welcomes Apollo Lupescu, Vice President of Dimensional Fund Advisors, a prominent global investment management firm to discuss the emotional and logical thought process associated with investing. Listen as Apollo delves into the distinctive investment approaches employed by Dimensional Fund Advisors, placing significant emphasis on their meticulous data analysis and their commitment to asset-class investing. The conversation also touches on the significance of effectively managing your investment expectations, the merits of diversification, and gaining a deep understanding of market probabilities.

Key takeaways from this episode include:

- The importance of asset class investing and understanding stock behavior

- Why managing your expectations is beneficial to your investment strategy, and your sanity

- Differences between a Bear and Bull market and how they can often be predicted

- Understanding that investing is mainly about grasping the concept of statistics and probabilities

- Why limiting how often you check the markets can produce a better outcome

- And more

Resources:

- Free Financial Resilience Assessment

- Stocks (1) at 9:37

- US – Domiciled Equity Funds at 12:33

- Stocks (2) at 13:08

- Growth in a Company at 20:33

- A History of Markets Ups & Downs at 28:48

- Watching the Market at 34:17

- Federer- Market Comparison at 38:56

- Apollo’s Notes [PDF of all slides]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Connect with Larry Heller:

- (631) 248-3600

- Schedule a 20-minute call

- Heller Wealth Management

- LinkedIn: Larry Heller, CFP®, CPA

- YouTube: Life Unlimited with Larry Heller, CFP®

Connect with Apollo Lupescu:

About Apollo Lupescu:

Apollo Lupescu is a Vice President at Dimensional Fund Advisors, where he started in 2004 after finishing his Ph.D. in economics and finance at the University of California, Santa Barbara. During his tenure at the firm, Apollo has gained experience in a wide variety of practical subject matters. He was part of the Dimensional Investment Strategies group, worked directly with financial advisors in the Northeast area to assist in the development of their business, managed the internal Client Services team that provides broad analytical support, and then oversaw the firm’s national advisor retirement business. He is currently Dimensional’s “secretary of explaining stuff.” In this role, he frequently presents around the country and the world at financial advisor professional conferences and individual investor events.

Prior to joining Dimensional, Apollo had his own consulting firm, which provided services to the US Department of State and the White House on a variety of projects. His interests in finance and investments led him to teaching engagements at the University of California, Santa Barbara. In addition to his Ph.D. from UCSB, Apollo has a BA from Michigan State University, where he competed in and coached water polo.

Publishing Tags: Life Unlimited, Podcast, Retirement, Heller Wealth Management, Financial Planner, Portfolio Management, Investment Management, Personal Finance, Wealth Management, CFP, Certified Financial Planner, Financial Advisor, Long Island, New York, Investing For Women, Business Exit Planning, Business Strategies

#LifeUnlimited #Podcast #Retirement #HellerWealthManagement #FinancialPlanner #PortfolioManagement #InvestmentManagement #PersonalFinance #WealthManagement #CFP #CertifiedFinancialPlanner #FinancialAdvisor #LongIsland #NewYork #InvestingForWomen #BusinessExitPlanning #BusinessStrategies

Transcript:

Voiceover (00:00:02) – Welcome to the Life Unlimited podcast with Larry Heller. You deserve complete financial advice so you can confidently live your life your way for life. Now let’s get into this week’s podcast episode.

Matt Halloran (00:00:19) – Hello and welcome to another Life Unlimited podcast with your host, Larry Heller. I’m Matt Halloran, the producer of the show. Today. We have a wonderful guest that I’m really excited to listen to, because I don’t know if you all know what Dimensional Fund Advisors are, but in the financial services world, they’re kind of a big deal. We’ve got Apollo, who is the vice president of Dimensional Fund Advisors, a leading global investment manager. He’s a renowned speaker, delivering hundreds of clear and engaging lectures to financial professionals and people like you, individual investors. With nearly two decades of dimensional funds and previous teaching roles at the University of California. And he also holds, I don’t know, something small, like a PhD in economics and finance from UC Santa Barbara and a BA in economics from the greatest state in the world, Michigan State University, which is where I am actually from.

Matt Halloran (00:01:06) – Apollo, I don’t know if you remember that, but before we turn it over to Apollo, Larry, how are you doing today? Are you ready to interview this juggernaut of a human being?

Larry Heller (00:01:14) – Yeah. No. I’m excited. I’m excited to have Apollo here. I’ve known Apollo a long time. He’s got a lot of things that our audience is going to want to hear. So I’m super excited.

Matt Halloran (00:01:24) – All right, well, Larry, I’m going to go ahead and turn it over to you, brother.

Larry Heller (00:01:28) – Thanks, Apollo, for joining us today. Like I just mentioned, I’m super excited and we’re going to get into a lot of different a lot of different topics. Now for my clients, they’re educated on who Dimentional is, but a lot of a listening audience out there that’s joining us for maybe even the first time. So why don’t we really start with the beginning and kind of tell this listeners a little bit about dimensional bonds?

Apollo (00:01:49) – Yeah. Well, first of all, hi, Matt. Hi, Larry. Great to see you. And thanks so much for the invitation to to be part of the webcast. I’m actually really excited myself to have this this conversation and dimensional funds. It is not a household name. It is an investment manager that is regulated pretty much like every other investment company in the US, whether it’s the SEC or Finra. But what’s interesting about dimensional is that, in my opinion, it’s the most successful cross-fertilization between the academic rigorous research and investing and the practical world where we live. And I think what’s remarkable is that a lot of the strategies, a lot of what’s being done is not any one person’s opinion, but rather this combined wisdom coming from analyzing data in a much, much more rigorous way than than we’re used to. Because this academic community is incredibly precise when it comes to data and evidence. So we’ve worked over the years with a number of Nobel winners, and they got the Nobel actually, after they work with dimensional. It’s not something that, well, we get the Nobel, let’s pay them so they can be on the associated with dimensional.

Apollo (00:02:57) – And secondly, I think what’s interesting is that we are not a typical fund. And pretty much like you, Larry, we are not in the business of selling our funds by paying commissions. In other words, we don’t operate in a way that encourages advisors to use us for the wrong reasons. Larry, for example, if you know he has thousands of mutual funds, ETFs and other investment products, and when he chooses something, it is not because they’re going to get paid for using that product. And I think having this business model that that kind of lines, Larry, in us, what it means is that there is no financial connection with the advisors using dimensional funds. And over the years, we have placed an incredible emphasis on working with advisors rather than directly with the investment public. We think that advisors are tremendously important to the investment process, whether it’s the planning aspect, whether it’s the rebalancing, the discipline that comes with working with an advisor. But we found that it’s much, much better.

Apollo (00:03:54) – The results are much, much better when an advisor is involved. And because of that, we don’t actually work directly with the investing public. And the third thing, that kind of sets dimension apart beyond the academic connection and the business model, is the fact that the strategies themselves are not in the typical buckets. Larry, as you know, there’s a bucket that’s called active management or traditional conventional Wall Street, which is basically either forecasting where the markets are going or trying to pick some stocks. And that’s one way of doing it. And the alternative is indexing, which is basically licensing a third party list provided by S&P or MSCI or other providers of these benchmarks or yardsticks of the market, and then just replicate it into a fun dimension is in neither of those buckets. It kind of stand alone, the fertile middle ground where we are trying to outperform, but not by picking stocks and not by trying to time the market, but rather in a much more rigorous and systematic way. So I say that for folks are not familiar with dimension like these three things the academic connection, the business model, and the uniqueness of the strategies are what sets dimension apart.

Larry Heller (00:05:02) – So there’s a lot of things there to to unpack. You know, let’s talk about the overall kind of business model. I remember probably over 20 something years when I first came across dimensional, being an accountant. From background in the analytic background, I had never seen any other type of funds out there that were developing models by the world of academia, that it was always your typical Wall Street person’s research on how to pick stocks or pick which sector is almost going on. So I came across this and saying, wow is how is this so different? And why is this a better way of investing long term for our clients? And, you know, a lot of people, the dimension doesn’t market out there. So they’re relying on the advisors and for us, and we’re free to use any of the funds. So just being able to use these strategies has been a game changer for myself as a firm and for our clients over the years. But let’s kind of look at what you started there talking about, because a lot of times trying to explain this, are you more active or you’re more passive and like you were saying, you’re neither.

Larry Heller (00:06:17) – So how can you be? How can you be neither? So why don’t you talk a little bit about maybe the models and how I’m not? You’re probably more passive than. Active, but you’re kind of doing both. And sometimes I say it’s, you know, it’s kind of maybe it’s a little bit of a mirror of an index with somebody driving the train out there. So why don’t you expand on that a little bit for us?

Apollo (00:06:40) – Yeah. So let’s let’s unpack because as you said, and I’m using some general terms and to some degree they can be confusing. So let’s start with the traditional the conventional way in which this business has operated. And I would say that that that model goes back to the days of Benjamin Graham. And it’s not a household name. But what’s important about Benjamin Graham is that he was one of the first investors to realize that, that when you deploy your capital, when you have money to invest, you’re basically in the market. You’re basically buying ownership into a company.

Apollo (00:07:12) – And what you need to do as an investor is do some analytical research onto the company that you’re buying, and be rigorous about understanding the numbers and whether or not that is a good deal to buy, given what you expect to get as a business owner down the road. And he created this idea of valuation and looking at companies. And actually, one of his students happened to be Warren Buffett and Warren Buffett, certainly better known than Benjamin Graham. But Warren Buffett credits a lot of his success to what he learned from Benjamin Graham. Don’t make investment decisions based on emotions or how you feel, or because your cousin Benny said that he should buy that, or because you think it’s a good idea. Do some homework, do some analytical when it comes to that company. And what emerged out of that is a style of investing where if, for example, this square represents the entire stock market, the idea is that if you look and analyze companies, you can cherry pick a handful of these companies that you think are absolutely the best investments, leave out everything else, and that’s going to make a lot of money.

Apollo (00:08:19) – And by doing that research, basically, Larry, what happens is that you are creating for yourself a competitive advantage. That’s the key insight when you’re buying shares of stock in Apple or GE or you name it, or Microsoft, you’re not buying that share of ownership typically from the company, you’re buying it from some other investor. So for every buyer there has to be a seller. And if you do your homework and you get information that is better, you can process it in a more efficient way, in a superior way, and where you can get the information fast, better information and faster. That gives you a competitive edge. That’s basically what Warren Buffett and Benjamin Graham have been doing and a lot of other managers. And it turns out that this conventional way has been sort of the cornerstone of how most investment funds in the US and across the globe are thinking about the way that to select investments, let’s analyze individual companies and and cherry pick what we think are the best ideas. The trouble with this is that it makes so much intuitive sense, and for the longest time it might have been fine to do.

Apollo (00:09:27) – But what I’m found over the past 20 years or 30 years that I’ve been in the industry is that the world has changed and the world has changed in a fundamental way, and it has to do with information. If you think about how quickly the information moves, it is almost instantaneous. Nobody can say, I can get information faster than everybody else. I think that’s delusional. Secondly, the level of information that exists has just absolutely exploded there. Companies who would take pictures of Walmart parking lots and sell to managers that the information of how many cars are in the parking lot this day versus a year ago. So they can get a sense if sales go up or down. The level of information is incredible, but also the competitiveness has changed to no to incredible degree, because today there are more professionally managed funds than actual stocks trading on the market. So for anybody who thinks that boy, you know, picking stocks is the way to go, just remember that. What is it that you know that other people don’t? Are you getting this information sooner than anybody else, which I doubt, legally speaking.

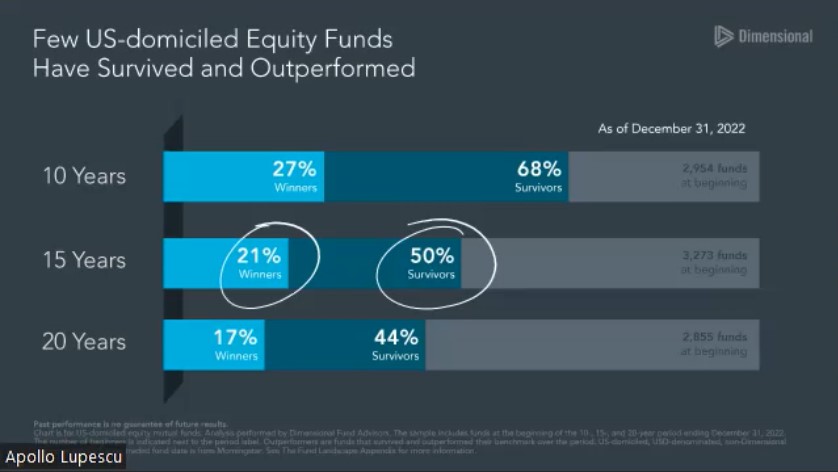

Apollo (00:10:37) – And thirdly, you are competing and for for the army of MBAs from Harvard, there is an army of PhD from Stanford, and there’s this tug of war. So what we found is that this particular way of investing money, this idea of stock picking, it is not state of the art anymore. And I don’t encourage people to do it. When you look at the data, what you find is that over ten years, if you look at a set of funds and he asked a question, how many of these funds even survived? Well, about a third of them, 32% disappeared. They didn’t even make it through the ten year period. And out of the ones that survived, only about 27% or so, it’s about 1 in 4 roughly outperform, meaning that three and four underperform. And the longer you look at this data, you look at ten instead of ten. Look at 15 years. It’s only about 1 in 5 funds. That’s. That that that outperform meaning that that 1 in 4 and five don’t.

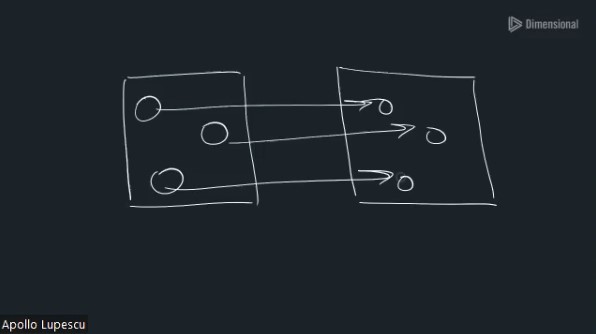

Apollo (00:11:31) – And look at the survival rate. It’s only half of the funds survive. You buy a fun and then roughly half of the funds that disappear. And if you look at really the 20 year, which is more in line with with sort of like my career, what you see is that only about 1 in 6 outperform five and six funds on the perform. So because of that, Larry, what we really believe is that this idea that that picking stocks, it is no longer state of the art. It might have made sense at some point. So that’s one set of funds and that’s not what dimensional does. So then what does dimensional do? What kind of research do you guys do there. Well, dimensional. And the academic community for that matter, started with the idea that you don’t want to love or hate anyone stocks. You certainly want to consider these stocks, but instead of trying to understand the behavior of these stocks by themselves, what you want to do is understand these stocks as part of a larger group, a larger basket of stocks.

Apollo (00:12:27) – And this has become known as asset class investing. The idea that I don’t love or hate anyone’s stock, but rather I’m interested in understanding that stock as part of a larger group. I try to explain this to my mother in law a while ago, and the closest thing that I can come up with is at the time when I went swimming in Florida, and as I was swimming, I had my goggles on and I looked down and there’s a school of fish, and every fish was moving so randomly up, down, left, right, sideways. No way you can predict how each individual fish should move. But once I started swimming a little longer with the school of fish, I started to capture and understand the behavior of the entire school of fish with a lot more precision that I could of anyone fish. And that’s kind of when it hit me what it is. Not about the fish, it’s about the school of fish. It’s not about the stock, because any stock can be random. But you want to understand the behavior of the entire asset class.

Apollo (00:13:22) – And that’s what dimensional has been trying to do. And this is what the academic community has been trying to do, is differentiate among these stocks, even as we know that the prices are fair because it’s so competitive. That doesn’t mean that all stocks have exactly the same potential for growth. And it’s been identifying these different patterns in the market. That’s been the really the interesting part. So what we found and this is going back to the 80s what this is where dimensional basically started the idea. One of the idea is that the dimensional promoted way back in the early 80s, was that the fact that if you look at the market, there are the distinguishing factor among stocks, and they don’t have to do necessarily with sector, which is what typically tends to be on the news, but rather one of the primary distinguishing factor has to do with the size of the company. And you have these large, well-established, mature companies that typically comprise, let’s say, the Dow Jones or the S&P 500. But in the US, they’re roughly about 2000 other stocks that are not part of the S&P, but they are still part of the market.

Apollo (00:14:28) – And these are called small caps or small company stocks. So Larry, let’s make it real. If you look at for example, let’s just make the poster child of of the large companies McDonald’s. So McDonald’s is a large, well-established company. It’s got track records, a lot of rigorous systems, all these things that that that make it what it is. Great company. Now in the stock market, there is another burger chain that is called Shake Shack. Some of the audience might be familiar with it. My kids are certainly familiar with that. And that is a publicly traded stock that is not in the S&P, but rather it’s a small company stock. So the question is, if you think of these two companies and you first ask the question, well, if these two stocks Shake Shack and McDonald’s, if you look at them, which one carries a little bit more uncertainty? Most people would say, well, Shake Shack is not as mature and robust as McDonald’s, on the other hand, which one can potentially grow and let’s say double in size.

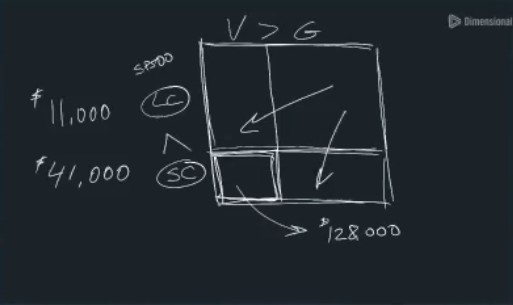

Apollo (00:15:26) – Well, most people would say, I can see Shake Shack doubling much more so than I can see McDonald’s. Its McDonald’s being so large and mature. So at that point, what’s interesting is to see from an investor perspective, what would have been the difference? Could you have made more or less money by differentiating these investment classes? And we have a book, Larry, that you’re very familiar with that you and I are going to we talked about this a lot. It’s called The Matrix Book. And in the matrix book, you kind of see the growth of a dollar going into these different investments all the way back to the 20s. And this is where these dimensional index come in very handy. So if you look at the S&P 500, a dollar going back to 1920s would have grown by the end of last year, which happens to be my dad’s lifetime. He was born in the 20s and passed away at 95 last year. In my dad’s lifetime, a dollar invested in the S&P would have grown to about $11,000.

Apollo (00:16:19) – Roughly speaking, that’s the ballpark. So it’s an amazing growth. One single dollar grows to 11,000 in. The large company in the S&P 500. The question is, if you had put the same dollar to work, but instead of buying the large school of fish, you buy the small companies. How would that be different? And when you look in the book and the matrix book and the dimensional small cap index, now what you see is that the same dollar over the same time period would have grown to about $41,000. So the idea being here is that that as an investor, you can have a you have a choice, you can buy these large, well-established companies. Or if you want to outperform the S&P, if you want to do better than the market can use. One of the things that he can do is start paying attention to the small companies as well. So what mention is really trying to do is identify these dimensions in the market and then provide advisors with funds that are very specific to each category.

Apollo (00:17:16) – So there’s a dimensional US large company and a dimensional US small company. There is a US or US international developed large and small. Everything is very targeted based on these dimensions, but large and small is not the only distinction. The only thing that really is important to know about that came up in the 80s, was the idea that among all the large and all the small, it really what we’re trying to do is distinguish. And what comes into play now is something that Benjamin Graham and Warren Buffett have been talking about, which is don’t just think about buying a company, but how much are you paying to own it? If you think of the price relative to some accounting fundamental that you can measure right now, and the lower priced stocks called value companies, over the long run they’ve outperformed the more expensive counterparts called growth. And that’s certainly in the data. So knowing that value beats growth small cap has outperformed large. Obviously the one part of the market that ought to give investors the biggest bang for the buck over the long run is small end value.

Apollo (00:18:17) – And what you see is that the growth of the same exact dollar over the same time frame in small value would have been a little over $128,000. So you look at the same time frame and a vastly different outcome. So what dimension is it really starts with this research and identifying these dimensions in the market, and then providing advisors with these funds that are very specific to each category. And the idea being that if you’d like to outperform the S&P, what you can do is emphasize, for example, small company stocks or value companies. And that gives an investor the chance to outperform in a much more systematic way than than just picking a stock. So you can still do better than the index and quite significantly. But I mean, look at the difference in these numbers. It’s quite staggering. And and but do it in a much more systematic way when you’re interested in the entire school of fish and not just individual companies. And now before I kind of.

Larry Heller (00:19:21) – Go ahead and a lot of this is really part of it is also about managing expectations.

Larry Heller (00:19:25) – You show that book there, which I still love to use because it shows. It gives clients and prospective clients some parameters on kind of the ups and downs on the one year basis versus the five, the ten, the 20, even the 50 year basis. So you can kind of say, hey, if we have X percentage in the small cap here, our expectations are this. And here’s the data to prove this versus other classes, the large classes and even the growth in the value. And what we do is obviously put together the asset allocation and the portfolios to have a little bit of everything, and we can blend it to what the risk and the time horizon for each one of our clients by having these specific types of funds. In other words, a fund that only does small cap value with small or large cap value, versus a manager that’s going to move from growth to value and from small to and from small to large. And it’s all about managing the expectations. Of course, we all know that sometimes some of these sectors are out of favor.

Larry Heller (00:20:33) – It doesn’t mean that they are bad. They’re bad funds are just add a favor for that. And we’ve seen we’ve obviously we’ve had some of these mega-cap growth who have had some extraordinary returns and had a, you know, how do you manage that? So being able to use dimensional being able to show from an academics gives people kind of a sense of, okay, this makes sense for my overall overall investment strategy. And I’m going to switch gears a little bit here. But hopefully that kind of explains to you out there the differences of what dimensional is. And it’s more than just an index. And we can outperform an index, but still not really try to be guessing and going from one stock to one stock to the other. When you were talking about your survival rate, I kind of remember Bill Miller. Forget the fun that he had. But I remember he was the really the only manager that outperformed his index, I think ten straight years. And then 2008 hit and he was overweighted into banking stocks and the fund closed a year or two after that.

Larry Heller (00:21:41) – I don’t remember the exact name of the fund.

Apollo (00:21:43) – I know exactly what he’s talking about. Add value in the name. But it was really.

Larry Heller (00:21:48) – It was really is really different. But I really.

Apollo (00:21:50) – Like the you know, just to wrap it up, the what you said in terms of the value of the advice, number one is put together these pieces because it’s very complicated to do it efficiently. In the US, international developed merging having an advisor to put it all together for you, it’s incredibly important. But secondly, exactly what Larry said having the discipline that at a time when something might doesn’t feel like it’s working out not to jump out because that might be the wrong time to do it. And most successful investors, they have a discipline. And that’s why we absolutely just we are we are so excited to work with advisors like Larry because of these two things. The exactly what he said, being able to to combine them efficiently, all these different asset classes, but also keeping clients disciplined. Right.

Larry Heller (00:22:35) – And we could talk about this for a long time. I want to switch gears for a little bit, but before before that, for those of you for our podcast is out there, we’ll be right back. But here’s a special offer for all of our listeners.

MIDROLL

And now we’re back to the episode. So let’s switch gears a little bit, because one of the things that I don’t care, and I’ve even done this with my clients and really thought, I’ve explained this and they come in and the first question is, well, what do you think about the stock market? Is it a good time? Should I get out? Should I get in? And there’s all different outside variables. Oh, interest rates are too high when we have the government debt problem. And now we have the Israeli war. I remember right before the election, Donald Trump and everyone, they don’t want to be in the market because they were afraid of what’s going to happen. And then he got elected in the first day.

Larry Heller (00:23:26) – Everyone remembers the market kind of tanked, and then after that it had the best November ever. So all these kind of things and all these, can you really get it right? Yeah. I guess there are people out there that are going to make some decisions and get it right out there. But why don’t you talk a little bit about some of these current topics that affect the market and our investment strategy? I’d love to hear your input on that.

Apollo (00:23:49) – Yeah. So I think it’s such an important question because I see that all the time. And and I think, Larry, I find it intuitively appealing. I want to. In fact, my wife is asking me like, you know, listen, it doesn’t look like things are going well. And there is this war. And just this weekend it was like, okay, it doesn’t seem should we pull the money out and maybe wait for this nuttiness to calm down and then put the money in back when it’s good to go and the market’s going to go up.

Apollo (00:24:17) – So what I find is that it’s very intuitively appealing to think that there’s a good time to be invested and that I should invest my money, and there is a time when I shouldn’t be invested and I have to get my money out of the market, and it’s intuitively appealing as it is. Well, we found over and over and what I found on my own, just money. There are some things that that you have to consider. The first thing to consider is that whether or not you need to be invested in the market, it is not a decision that that comes out of nowhere. It is actually it depends. It depends because what really matters is the financial plan. So I cannot tell anybody that you should be invested or not be invested, because you need to have a financial plan. And that financial plan looks at your circumstances, your assets, winning the money. How much money do you need? What is your risk capacity? What can you sleep at night? And then based on that plan, it determines what proportion of your assets of your money should be invested in the stock market.

Apollo (00:25:19) – And perhaps what proportion should be invested in other assets, like for example, a bond, which is a type of a loan that is a stated interest rate that you receive, and what’s the balance between those? And for some people, it is quite possible that the preponderance of their money, the majority of the money, might need to be invested in bonds, not as much in stocks. So I couldn’t tell you that unless you have a plan. And that’s what Larry and the team do. They create these plans and then they can decide what percentage should go in the stock market. But for the portion that you should have in the stock market, is that something that, you know, how should you think about that? Should it be invested? Well, it turns out that if you look at the stock market, we are dealing with some issues right now that’s really seem huge. As you said, we have a war in Israel right now. We have Ukraine. I mean, we have the issues with China, all these things that are happening at the moment.

Apollo (00:26:13) – And at the same time, when you look historically, the world in some shape or form, it always had issues. This is not the first time we’ve in fact, we had some even bigger issues. You have World War Two when you had millions of people dying. The whole world was pretty much on fire. So we have seen other times. Larry, you remember three years ago, not 30 years ago, we were all stuck at home without the ability to leave. We couldn’t go anywhere. And that was tough. So there’s so many things that happen in the world. And in fact, if you look at the history of the stock market and it’s so interesting and you do a timeline of the market based on the ups and downs, and you can differentiate between bull markets and bear markets, bull market, obviously the market goes up, bear markets, it drops by about 20% or so. Which, you know, going back in the timeline of the markets, the two things that jump at me when you when you really look at the ups and downs in the market through bull and bear markets, the first thing that you see is that the bear markets absolutely happen.

Apollo (00:27:14) – And it’s something that that you should expect. You should expect that at times the market’s going to drop. So when the market drops it’s nothing unusual, nothing unprecedented. But what’s interesting is that the bear markets do not last nearly as long as the bull markets. That’s really important. And you see here how much longer the bull markets last. But the second thing that you see is that how unpredictable these bear markets are, they don’t at at in a pattern that you can identify to say let’s jump out of the market. In fact, they happen at really random times. And what we found in talking to investors is that if one decides that, hey, listen, I need to get out of the market because I see there’s a bear market come. What we found most often is that the biggest issues investors have is that if they leave the market, they have to make an equally important decision, which is when do they get back in the market. And making these two correct decisions is, I don’t know anybody who can consistently make these two correct decisions, but what I’ve done is met enough people who are basically they basically replace the stress of being in the market with the stress of being out of the market.

Apollo (00:28:29) – I can’t tell you when the market tanked with the pandemic, how many folks said, I’m done, I need to get out because this is scary. And they sold after the market dropped, and then they saw the market rebound and come back and they’re sitting in cash after paying the taxes down on the gains, but they’re sitting in cash panicking and stressing out. When do I get back in the market because I’m missing the rebound. So making these two correct decisions is nearly impossible.

Larry Heller (00:28:55) – And making almost nothing on interest rates.

Apollo (00:28:57) – Exactly. You’re making nothing and just sitting there. So what’s the idea? The first thing is that you might not need to have all your money in the market. A portion of your money might be invested in bonds and even might be invested in international stocks, emerging market stocks. The second thing is that understand that the nature of the markets is to fluctuate, and the markets have seen craziness in the world before. But what we found is that the bear markets don’t last as long as the bull markets.

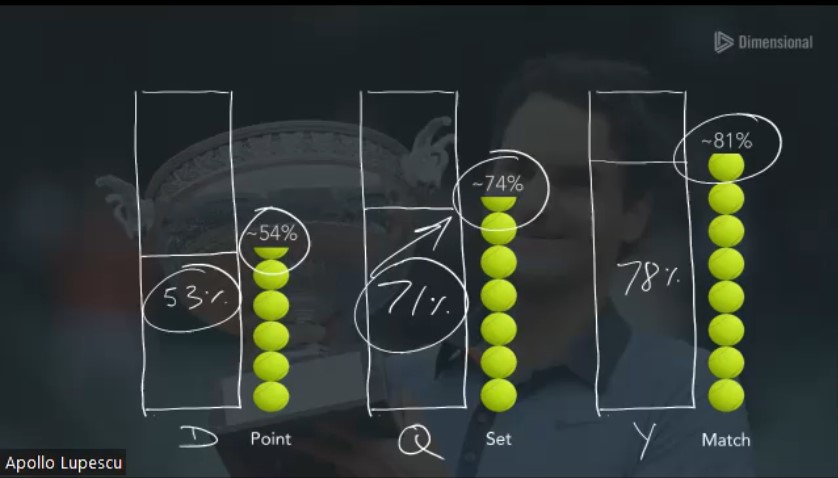

Apollo (00:29:23) – But thirdly, I like to think in this academic term that life in general, not just investing, it is not about certainty or guarantees, but much more about understanding odds, statistics and probabilities. And that’s kind of how I see the world, everything investing, including investing and what I mean by that, well, a lot of folks are paying attention to what is going on in the market on a daily basis. Again, my my father in law is talking about family members. He does it. He watches every day what happens in the market. And I can see that sometimes, you know, he’s happy, sometimes is not happy. And he kind of like slumps out. And I wanted to know, just out of my curiosity, what is the split between positive and negative days in the market on a daily basis? So if you go to Yahoo Finance, where you can go to any website and you look at the daily one over the last few years, the last 50 years for that matter, on a daily basis, which is that the S&P 500, roughly 53% of the trading days, has gone up, meaning that 47% is not.

Apollo (00:30:27) – So if you watch the market on a daily basis, be prepared to be disappointed roughly half the time. That’s been the norm. So watching the market daily, it’s a little bit like a flip of a coin. It’s not obvious that you make money. You have a little bit better odds to make money, but I can tell you they’re overwhelming. It’s a bit of a flip of a coin. So to me, being in out of the market on a daily basis, it costs money. They’re taxes. But it’s not obvious that you make or lose money. Now what if you change your horizon? You just simply change your framing of time and instead of watching the market daily, you want you wait for the quarterly statement. And which happens then if you wait for the quarterly statement, what you see now is that roughly about 71% of the time in any given quarter, historically, over the past 50 years, you would see a positive outcomes. You’ve made money and about 29% you did not. So simply switching from daily to quarterly, you are a lot more likely to see a positive outcome.

Apollo (00:31:34) – And from quarter to quarter things are random. But here’s a question for you folks. If you were to stay out of the market for one quarter, what is it more likely for you to miss a good quarter or a bad quarter? You can certainly miss a bad quarter and pat yourself on the back and say, great, I saved myself money, but in reality, you are a lot more likely to miss a good quarter. Would you ever play a game? Would you ever sit at a table? Will you play a game and you lose 71% of the time? Because that’s exactly what happens when you say, I’m going to get out of the market. And the longer you wait, the worst your odds become. When you look at an annual basis over the past 50 years, what you see is that roughly about 78% of the time the market’s gone up and only 22% has gone down. So, Larry, to me, this idea is that the last idea is that investing when you’re investing is about the long run.

Apollo (00:32:29) – It doesn’t have to be the super long run, but it just can be daily. You have to give the market some time. And I was so in.

Larry Heller (00:32:38) – And that leads right to what we do when we talk about planning and we talk about expectations. So that your charts there is, you know, framing it in the communications of that. And that’s exactly what we do, especially if you’re retired and pulling money out. When we looked at your bull market for your bear market, if we can have enough short term now cash or even short term treasuries to ride out your short term time frame, we call it our short term reservoir. And maybe your intermediate is reservoir is maybe with bonds. But your long term reservoir is that as equities. And now you’re taking away not having to worry about turning on the TV every day whether it’s up or it’s down, because we’ve basically, you know, told our clients that that part, that reservoir is really long term. And now you’re more likely to have higher rates of return over the long term.

Larry Heller (00:33:31) – And you’re not worried about the day to day, the quarter to quarter as as much because you know that’s going to happen. So a lot of this is why we’ve kind of aligned. Some of the strategy with dimensional is really managing expectations and seeing what that is and not trying to outperform on a daily basis or a or a stock picking preservation. Some people are going to get it and some people are just want to have that home run, want to have that stock, want to have that excitement of that versus, okay, I’m in a small cap value fund and maybe I’m rebalancing a little bit here. So all these type of things when when somebody’s an investor gets it and a light bulb goes off, they’re not worrying about that and they can get it and they cannot stop worrying. And that’s really what our job, if they can stop worrying about it and get the returns that they need, I’m doing my I’m doing my job. So this has been great. Some of these charts and communications are going to be super helpful to our audience out there. Apollo, any final thoughts that you might have.

Apollo (00:34:31) – Yeah, I mean, exactly what you said is like, you have to be able to have some peace of mind. And and I had this, I had this, this, this conversation at a retirement community in Northern California and the folks there, basically they’re watching the market daily. And they’re also, you know, the two things they did is watch the market and play tennis. And one of the questions was, are these odds enough? Is this going to make me a successful investor? If I really look at these odds? And what was interesting to me is that I was able to look up a statistic that hopefully help them understand that the odds and how to think about that and winning and investing and and it kind of I don’t know if you know this, this young fellow who’s probably not as young these days, but maybe people might recognize him.

Larry Heller (00:35:15) – Yeah, sure we do.

Apollo (00:35:17) – Roger Federer, he’s, you know, arguably one of the, if not the best tennis player.

Larry Heller (00:35:22) – Or maybe the second best now,

Larry Heller (00:35:24) – maybe the second. Best. Yeah.

Apollo (00:35:26) – So what was interesting, Larry, is that I had this thought, okay. So if you look at Roger Federer, arguably one of the top three best players of all times in tennis, I wanted to know what percentage of the balls that he plays, the points that he plays. Does Roger Federer win? And what was interesting is that if you look at the statistics, what you see is that he wins roughly about 54% of the points that he plays, meaning that that about 46%, roughly half the points that Roger plays. He loses, he loses roughly half the points. And yet you don’t have to panic, because if you give Roger some time, when he looks out at sets, he wins roughly 74% of the sets that he’s split in his career. And then if you give him even a little bit more time and you look at the matches, he wins roughly 81% of the matches. In other words, if you look at the comparison with the statistics that I just put up in the stock market on a daily basis, it’s 53.6, Roger’s is 54.1.

Apollo (00:36:35) – So to me it’s like don’t panic. If any given day Roger doesn’t win a point or the market doesn’t go up. We know that roughly half the time both Roger Federer and the market roughly have the time will lose. But if you give them time and now instead of looking at a point, you look at a set, you once again, you see that, hey, you know what? My odds are improving. I’m more likely to see the outcome that I expect. And the more you give time. Both in the market and to Roger. That’s how you see the outcome. So can you become a champion with these percentages? Roger Federer is one of the all time best. So I’m not giving you an average player. I’m telling you that when you look at the all time, the way you win championships is not by winning every single point. You win roughly half. But a lot of times the key element here is that you win the key points. And that’s why it’s the same in the market.

Apollo (00:37:31) – Key points in the market means that you have to be invested in those days when the market really takes off. And a lot of these are kind of like the key points that Roger won in his career. But again, give Roger some time, give the market some time. And that’s how you become a champion.

Larry Heller (00:37:47) – Oh I love that. What a great analysis between Roger Federer and a market. I hope everyone out there has enjoyed this. Apollo thank you so much I love this. We can talk for another hour or so but but thanks again for being here. Thanks again for the audience. Matt I’m going to throw it back to you.

Matt Halloran (00:38:04) – Fantastic. Well, Apollo, Larry, that was wildly informational. And for those of you who were listening to this as a podcast, only you got to check out the YouTube video, because Apollo was like doing all sorts of super cool stuff with slides and a whiteboard, and there were some wonderful, wonderful visuals. So listen, if you know anybody who hasn’t had the chance to really find out what it means to have a life unlimited, please make sure that you share this podcast with your audience.

Matt Halloran (00:38:29) – Now, Apollo, if anybody wants to know more about who you are and what you do, what should they do?

Apollo (00:38:34) – Well, I think the best thing is DFA US dot com that’s the website. But really, as I said, it’s informational, just general knowledge. We don’t work directly with individual investors. And so probably the best thing is actually go to Larry’s website, because that is truly the place to to get more information on how to implement these strategies in somebody’s life, they can.

Larry Heller (00:38:54) – Reach us, said Heller Wealth Management. Or feel free to give the office a call at 631-248 3600.

Matt Halloran (00:39:02) – And Larry, you also have an offer on the website. You want to talk about that real quick?

Larry Heller (00:39:06) – Yeah. So for those of you we’ve added on the website are a financial resilience quiz. So so I mentioned that a little bit earlier in the middle of the podcast about how you can take that quiz. So we have that up there. It’s totally free. If you want to get a little bit more idea of where you think you fit, you answer a few questions and we’ll be able to give you some idea on your financial resilience.

Matt Halloran (00:39:26) – Fantastic. We will make sure we have links to all of those things in our show notes. So for Apollo and Larry, this is Matt Halloran. And we’ll see you on the other side of the mic very soon.